234A & 234B Interest Calculator

234C Interest Calculator

File Your Income Tax Return Now

Infinite Referral Program: Get direct cash in your bank every time your referee makes a purchase.

234A of Income Tax Act: Interest Penalties u/s 234A, 234B & 234C

Types of Interest Under Section 234a

With proper planning, one can maintain timely tax payments. However, if not planned on time, you might end up delaying your payments.

There are 3 types of interest covered under section 234:

- Section 234A of the Income Tax Act for delays in filing income tax returns.

- Section 234B of the Income Tax Act for delays in the payment of the advance taxes.

- Section 234C of the Income Tax Act for postponed payments of advance taxes.

Let us have a look at all of them in detail.

1. Section 234A – Interest for Default in Filing Tax Return

The interest levied for delay in filing the return of income comes under section 234A of the Income Tax Act. If the taxpayer files their income tax return after the due date specified by the authorities, an interest under this section will be levied.

Let’s assume Mr.X has an outstanding amount of ₹2,00,000, which includes his net advance tax plus TDS. Now, instead of November 30, 2020, he files his returns on May 15, 2021. He is hence, late by six months. His interest will thus be:

2,00,000 X 1% X 5 = ₹10,000

Mr.X will now pay an additional ₹10,000. If he continues to not pay his dues even further, an additional interest of 1% will be added every month.

- Rate of Interest under Section 234A: Interest u/s 234aA is levied for delay in filing the tax return of income. Interest is levied at 1% per month or part of a month on the tax amount outstanding. The interest that needs to be paid is simple interest. The taxpayer is liable to pay a simple interest at 1% per month or part of a month for delay in filing your tax return.

- Period of Levy of Interest: Interest u s 234a starts right from the date immediately following the due date of filing the income tax return, and ends on the date of furnishing the return of income. In cases where no return has been furnished, the interest starts to build up until the date of completion of the assessment under Section 144.

- Amount on which Interest is to be Levied: In case of delay in filing of income tax return, interest shall be liable to pay on the amount of the tax on the total income as determined under sub-section (1) of section 143, and where a regular assessment is made, on the amount of the tax on the total income determined under regular assessment, as reduced by the amount of

- Advance tax, if any paid

- Any tax deducted or collected at source

- Any relief of tax allowed

Example: The tax liability of Person-A for the financial year 2019-20 is amounted to ₹8,400. In his case, the due date for filing the return of income is 31st July 2020. He paid a tax of ₹8,400 and filed his return on the 5th August 2020. Is Person-A liable to pay interest under section 234A? Yes, Person-A will be liable to pay interest under section 234A for a month at the rate of 1%, on the outstanding tax liability as he has made a delay in filing the return of income.

2. Section 234B: Interest for Defaults in Payment of Advance Tax

Interest u s 234B of the Income Tax Act is levied in two cases - 1) If the taxpayer has failed to pay advance tax, which he is liable to pay if his estimated tax liability for the year is ₹10,000 or more, or 2) If the advance tax paid by the taxpayer is less than 90% of the assessed tax, which is the amount of tax as calculated under section 143(1) and where regular assessment is made, the tax on the total income determined under such regular assessment.

Let’s retake the example of Mr.X, and assume that he has a payable tax amount of ₹1,00,000. The TDS calculated is ₹82,650. This makes the Assessed Tax (1,00,000- 82,650) = ₹17,350. He should’ve paid a minimum of ₹15,615 (90% of ₹17,350) by the 30th of June, 2020. However, let’s assume he had paid only ₹6,000 on the due date and the rest on November 15, 2020.

Now, he will pay the following interest.

₹15,615 X 1% X 5 months (delay) = ₹781 (rounded off)

- Rate of Interest under Section 234B: Interest under 234B is levied for default in payment of advance tax. Interest is levied at 1% per month or part of a month. The interest that needs to be paid is simple interest. The taxpayer is liable to pay a simple interest at 1% per month or part of a month for default in payment of advance tax.

- Period of Levy of Interest: Interest under section 234B is levied from the first day of the assessment year (mostly from 1st April) till the date of determination of income under section 143(1) or when a regular assessment is made. In cases where the income is increased basis of the assessment or re-computation, the interest is levied on the differential amount from the first day of the assessment year till the date of assessment or re-computation.

- Amount on which Interest is to be Levied: The taxpayer is liable to pay interest on the amount as follows:

- If the taxpayer has failed to pay advance tax, on the amount equal to the assessed tax, or

- If the advance tax paid by the taxpayer is less than 90% of the assessed tax, the amount by which the advance tax paid as aforesaid falls short of the assessed tax.

Example 1: Monica’s total tax liability was ₹50,000 in the previous year.

She paid her income tax on 15th July during the ITR filing

There was no TDS deduction

But since her total tax liability was more than ₹10,000, she was liable to the advance tax. However, she didn’t pay the advance tax

Hence, now Monica has to pay the interest u/s 234B of the Income Tax Act

Here is the amount of Interest she has to pay:

50,000 x 1% x 4 (April, May, June, July) = ₹2,000 is the amount of interest Monica has to pay towards interest under section 234B.

Example 2: Manav had a total tax payable of ₹50,000.

Out of this, he paid ₹44,000 on 29th March as the advance tax. He paid the remaining ₹6,000 while filing his income tax return on 30th May.

Now, you can see that he has paid less than 90% of the assessed advance tax. The assessed tax is ₹56,000, which is ₹45,000.

Hence, Manav has to pay the interest under section 234B.

Here is the amount of interest he has to pay:

Difference between assessed advance tax: 50,000 (assessed advance tax) – ₹44,000 (advance tax paid) = 6,000

Interest to be paid: 6000 x 1% x 2 (April and May) = ₹120 is the amount payable towards the interest under section 234B.

3. Section 234C: Payment of Advance Tax not on Time or Interest for Deferment of Advance Tax

Section 234C of the Income Tax Act defines the rate of interest and conditions if you delay the advance tax instalments. Everyone, including salaried taxpayers, is required to pay advance tax every quarter of the financial year.

If your advance tax instalments have been delayed, you are required to pay a penalty as defined in section 234C of the Income Tax Act. Interest under section 234C is levied in case of deferment of different instalments of advance tax in the following cases:

- For taxpayers other than those who have opted for a presumptive taxation scheme under section 44AD or section 44ADA, interest shall be levied-

- If the advance tax paid on or before the 15th day of June is less than 12% of the tax payable on the returned income,

- If the advance tax paid on or before the 15th day of September is less than 36% of the tax payable on the returned income,

- If the advance tax paid on or before the 15th day of December is less than 75% of the tax payable on the returned income and

- If the advance tax paid on or before the 15th day of March is less than 100% of the total tax due on returned income.

- For taxpayers who have opted for a presumptive taxation scheme under section 44AD or section 44ADA, interest shall be levied if the advance tax paid on or before the 15th day of March is less than 100% of the tax due on returned income.

- Rate of Interest under Section 234C: Interest under Section 234C for default in payment of instalments of advance tax is levied at 1% per month or part of a month. The taxpayer is liable to pay a simple interest at 1% per month or part of a month for short payment/non-payment of individual’s instalments of advance tax.

- Period of Levy of Interest: Interest under section 234C is levied for a period of 1 month in case of a shortfall in payment of the last instalment and for a period of 3 months in case of a shortfall in payment of the first, second, and third instalments.

- Amount on which Interest is to be Levied: The taxpayer shall be liable to pay interest on the shortfall of advance tax on respective individual installments in case of shortfall therein.

Late payment interest under this Section, too, is applied at the rate of 1% on the outstanding amount of tax, starting from the individual dates listed above up to the payment date.

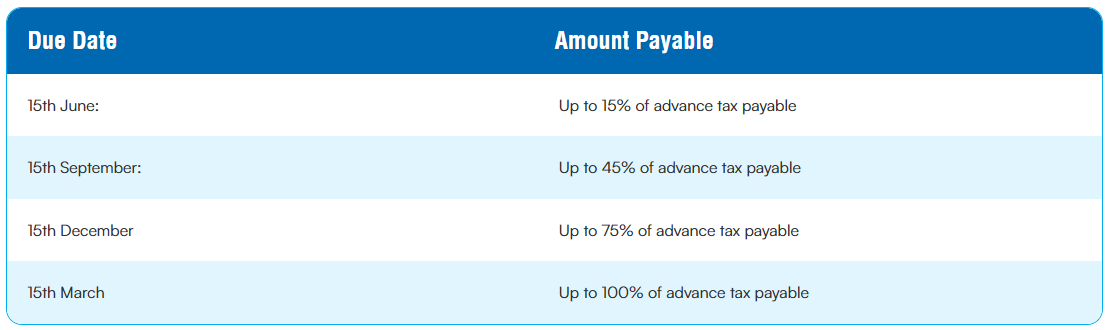

How to Calculate Interest under Section 234C?

First of all, you need to know the amount of advanced tax you need to pay every year before the due date:

How to Calculate Interest under Section 234C?

First of all, you need to know the amount of advanced tax you need to pay every year before the due date:

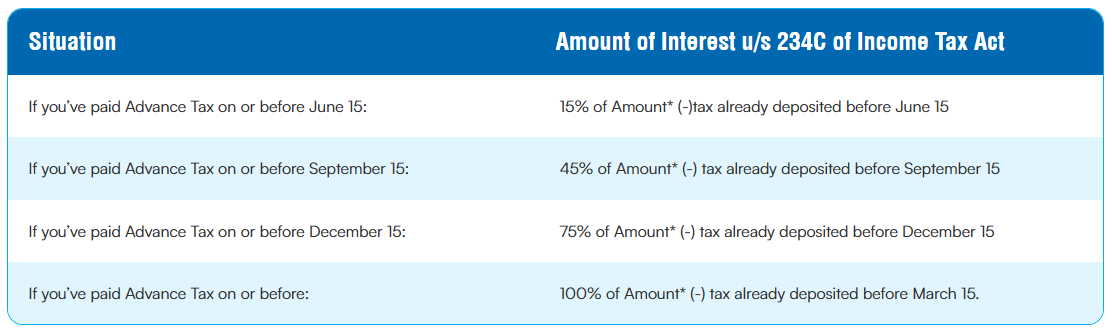

Amount of interest payable of Advance Tax under section 234C of Income Tax Act is less than the assessed amount:

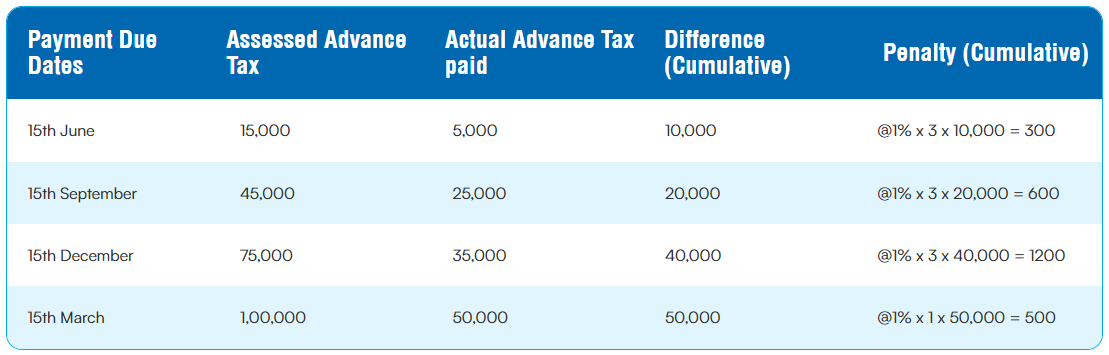

Calculation of Interest for Late Payment

Summing Up

It is important to know details about these sections, but what is more important is keeping track of due dates and making payments on time. To reduce your tax liability, there are always life insurance and other instruments that add value to your savings.

Frequently Asked Questions